Services de conformité

Nous assistons à une explosion mondiale de la législation sur la facturation et les bons de commande (déploiements gouvernementaux), ce qui constitue un défi de taille pour les entreprises. Comment rester en conformité de manière rentable et éviter des amendes coûteuses pour non-conformité ?

Les dernières informations à l’échelle mondiale

B2G e-invoicing mandate delay

We have previously communicated on the B2G e-invoicing mandate in Slovakia, where e-invoicing has been gaining significant momentum.

Slovakia has announced a slight delay to its B2G e-invoicing mandate, which is now expected to start in April 2023 as opposed to January 2023.

VAT rate increase

We recently communicated that Swiss government were intending to increase VAT rates in the country, for the reasons outlined here. The Swiss government has now confirmed the change in VAT rates in line with the following:

- Standard VAT rate from 7.7% to 8.1%

- Reduced VAT rate from 2.5% to 2.6%

- Special rate for accommodation services 3.7% to 3.8%

The increase will come into effect on 1 January 2024.

Further information around the VAT rate increase is expected from the Swiss tax authorities before the implementation of the change.

Update on penalties for e-transport requirements for high fiscal goods

We recently communicated that the penalties for non-compliance in respect of the e-transport requirements for high-fiscal goods in Romania were delayed until January 2023.

The Romanian Ministry of Finance has now officially confirmed this via the following link:

https://mfinante.gov.ro/documents/35673/5553347/proiectOUGmodifcompletactenormative_21092022.pdf

Temporary reduction of VAT rates

Inflation is spiralling across Europe, compelling multiple government to closely scrutinise their fiscal policies. While typically this year we have seen governments target niche VAT rates, such as energy, gas or food, some governments are making more radical changes by overhauling their standard and reduced rates.

Luxembourg is one such country – due to inflation standing at 6.9% in September 2022, it has been driven to review its tax measures. To this effect, Luxembourg has now announced a temporary decrease of the standard, intermediary and reduced VAT rate applied to goods and services, in line with the following:

- Standard rate: from 17% to 16%

- Intermediary rate: from 14% to 13%; and

- Reduced rate: from 8% to 7%.

- The super-reduced rate will remain unchanged at 3%.

These rates will apply from 1st January 2023 to 31 December 2023. It is expected that the VAT rates will return to their original rate at the start of 2024.

Tungsten is compliant in Luxembourg and supports all valid VAT rates in the country. Tungsten will ensure the new VAT rates are integrated as part of our solution once effective.

Compilation Guide update

The Italian tax authorities previously released a new version, 1.7.1, of the Compilation Guide for electronic invoicing and the Esterometro, which updated Annex A of the technical documentation for B2B e-invoicing. This outlined further detail around document types TD17, TD18 and TD19 in Italy.

The Italian authorities have now released version 1.8 of the Compilation Guide regarding the Electronic Invoice and Esterometro. This includes the following changes:

- Further information relating to a new document type, TD28

- Further clarity around the usage of an existing document type, TD19.

Tungsten Network has successfully enabled the new document type TD28.

These changes have taken effect from 1 October 2022.

The new documentation can be found via the following link:

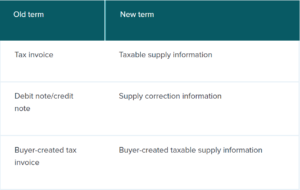

Upcoming changes to GST invoicing in New Zealand

The Inland Revenue of New Zealand is introducing a set of new rules around tax invoices, with effect from 1 April 2023. Here is a summary of the key points:

- New terminology:

Note that: businesses will not be required to change the wording on their tax invoices to reflect the new terms.

- Date for providing taxable supply information to the buyer

Sellers must provide their buyers with the taxable supply information within 28 days (or by an alternative date agreed by both parties) of a request for supplies over NZ$200.

In the case of supplies under NZ$200, sellers must keep a record of the supply, but are not required to provide taxable supply information.

- Physical record keeping is no longer required

There will be no need to maintain a single physical document containing supply information, such as a tax invoice, credit note, or debit note. All the information you need to support your GST returns may be contained in your transaction records, accounting systems, and contract documents.

- Providing Supply correct information

In the case of an incorrect amount of GST being included in the taxable supply information (currently called tax invoice), or when the seller has included an incorrect GST amount in their GST return, supply correction information (currently called credit notes or debit notes) must be provided.

Also, the Inland Revenues encourages business to adopt PEPPOL e-invoicing and has published a list of registered software providers at eInvoicing Ready product register | ATO Software Developers

ZATCA proposed amendment on Article 33 of the VAT law

Zakat, Tax and Customs Authority (ZATCA) released draft legislation proposing an addition to Article 33 of the VAT regulations, which includes a zero VAT rate for “exporting” services.

The following amendment has been proposed by ZATCA to Article 33 of the VAT Implementing Regulations:

“3- Notwithstanding the second paragraph of this article, the supply of services to a non-resident customer in any of the member states is subject to the zero rate in cases where the supply facilitates the supply of taxable services by that non-resident customer to a person in the Kingdom.”

Stakeholders and taxpayers were encouraged to share feedback on this proposal no later than 11 November 2022.

ZATCA releases user manual for Fatoora portal user manual – Version 2

ZATCA has published a user manual for accessing the Fatoora Portal to onboard taxpayers’ E-invoicing Generation Solution (EGS) units. The user manual provides information on the following:

- Accessing Fatoora portal through the Taxpayer credentials to generate the OTP (one time password) as part of EGS onboarding process.

- Generation of OTP for the renewal of the existing cryptographic stamp identifier (CSID).

- Viewing the list of onboarded solutions and devices along with option to revoke an existing EGS units.

- E-invoicing statistics which provides a summary of the statistics in relation to the submitted documents in the past 12 months along with their respective status.

- API Documentation link that can be used to access the ZATCA developer portal.

You can access the English version of the guide on the ZATCA website: https://zatca.gov.sa/en/E-Invoicing/Introduction/Guidelines/Documents/Fatoora%20portal%20user%20manual.pdf

E-Invoicing threshold reduced to ₹5 from January 2023

The GST Council has mandated e-invoicing for all businesses with turnovers exceeding Rs 5 crore ($630,000) starting from 1 January 2023. This means that All GST registered businesses that meet this threshold must integrate their systems and clear their invoices with the government portal before sharing with their buyers.

Accordingly, the Council has requested technology providers to ensure that the portal is ready by the end of December to accommodate the increased volumes of transactions.

Tungsten has supported the e-invoicing mandate since its introduction in 2020 and is prepared to accommodate this new threshold change.

Proposal of exempting VAT from basic goods

In a recent bill (House Bill-5504), the House of Representatives urged the government to exempt basic goods from VAT, including bread, raw and refined sugar, canned goods, instant noodles, biscuits, cooking oil, salt, laundry detergents, firewood and charcoal, candles, and drugs labelled “essential” by the Health Department.

HB 5504 aims to ease the economic burden of rising prices and a falling peso for ordinary Filipinos. As lead representative of this bill, Arlene Brosas, Assistant Minority Leader, pointed out that: “Removing the 12-percent VAT on basic goods consumed by poor families on a regular basis will dramatically ease their economic suffering amid skyrocketing prices, massive joblessness, and depressed wages”.

Additionally, she noted that the revenues lost under the proposed VAT exemption could easily be recouped by imposing a wealth tax on the wealthiest Filipinos.

Déploiement allemand

Déploiement allemand Déploiement indien

Déploiement indien